Property Market Forecast 2026: Yields, Growth & Opportunities

As the UK property market moves towards 2026, investors are confronted with a landscape defined by both opportunity and caution.

Following years of volatility, including sharp fluctuations in interest rates, changing tenant preferences, and economic uncertainty brought about by inflationary pressures, the market is stabilising, though unevenly across sectors and regions.

London remains a stronghold for prestige investment, providing capital preservation and long-term stability, yet northern cities such as Manchester, Liverpool, Leeds, and Newcastle are increasingly drawing attention. These cities offer higher rental yields, robust tenant demand, and ongoing urban regeneration, making them attractive alternatives for both domestic and institutional investors.

This report provides a data-driven, investment-focused deep dive analysing economic conditions, regional trends, sector performance, and strategic insights. The report will provide a comprehensive understanding of where opportunities lie in 2026 and how to navigate a market shaped by both traditional drivers and emergent trends.

1. National Market Trends

1. National Market Trends

1.1 Macroeconomics: An Overview

The UK economy in 2026 is projected to achieve moderate growth, reflecting stabilisation after a period of heightened volatility. GDP growth is expected to be uneven, with London continuing to dominate in commercial recovery, while northern cities maintain steady residential demand.

Inflation, which peaked in the early 2020s, is anticipated to ease slightly, yet energy and construction costs remain elevated, influencing both development expenditure and returns on investment. Mortgage rates have stabilised after rapid increases, presenting an opportune moment for investors seeking to expand portfolios or enter new markets.

A closer examination of the macroeconomic landscape reveals that northern cities are benefitting from structural changes. Urban regeneration projects, increased investment in digital infrastructure, and the migration of young professionals from London have created pockets of strong demand for both residential and commercial properties. Meanwhile, policy shifts aimed at stimulating housing supply in regional areas are expected to bolster long-term stability and investment confidence.

1.2 Residential vs Commercial Investment

In the residential sector, city-centre apartments, student accommodation, and properties in commuter towns continue to attract strong interest.

Demand is being driven not only by young professionals seeking proximity to employment hubs, but also by overseas students and graduates who see the UK as a long-term base. Institutional investors are particularly drawn to northern cities, where rental yields remain comparatively high and capital appreciation prospects are promising.

Cities such as Manchester, Liverpool, and Leeds are benefiting from demographic growth, infrastructure upgrades, and strong employment pipelines in technology, healthcare, and education. The expansion of build-to-rent schemes further reinforces this appeal, providing tenants with flexible leasing options, on-site amenities, and professional management services, while offering investors predictable, stable returns and the ability to scale portfolios across multiple urban markets.

Commercial investment remains selective, with investors focusing on assets that balance resilience with growth potential.

Grade A office space, particularly in northern hubs such as Manchester and Leeds, is demonstrating potential for both rental income and long-term appreciation, supported by occupier demand from high-growth sectors including financial services, digital, and life sciences. Well-located developments with strong ESG credentials are seeing greater competition, as occupiers increasingly prioritise sustainability and energy efficiency in their leasing decisions.

Retail investment, meanwhile, remains concentrated in prime city centre locations where footfall is consistent, tenant mix is diverse, and redevelopment opportunities exist. Secondary high streets, however, are experiencing slower growth and structural adjustment, with vacancy rates elevated and local authorities exploring regeneration strategies to restore vibrancy.

This divergence between sectors requires investors to carefully weigh yield potential against risk, particularly as hybrid working arrangements reshape office demand and e-commerce continues to challenge traditional retail models. Forward-looking investors are increasingly considering mixed-use schemes that combine residential, retail, and office elements, helping to future-proof assets in an evolving market.

2. Regional Deep Dive

2.1 Northern Powerhouse

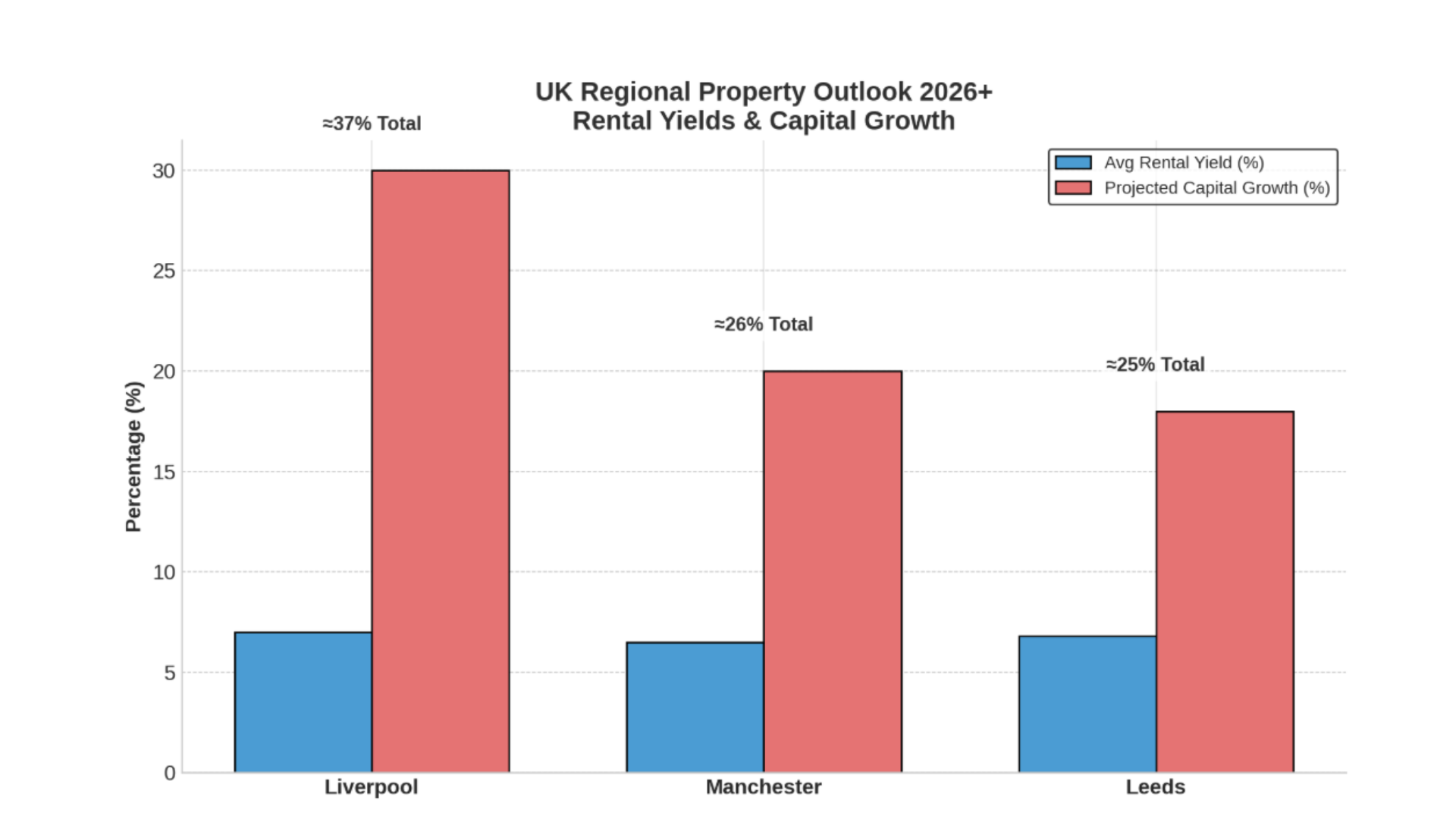

Manchester, Liverpool, and Leeds exemplify the emerging opportunities outside London. Accelerated rental growth is being driven by the expansion of digital and professional service sectors, student populations, and urban regeneration projects. These cities offer a balance of yield and capital appreciation that is increasingly attractive compared to London, where high acquisition costs limit potential rental returns.

Investors should note that northern cities benefit from high tenant demand driven by students, professionals, and regional migration. The combination of relatively affordable property prices, ongoing regeneration projects, and well-connected transport infrastructure makes these cities particularly compelling for medium to long-term investment. Market analysts predict that the next five years will see steady rental growth in these cities, outperforming national averages while mitigating exposure to London’s high entry costs.

2.2 London and South-East

London continues to command attention due to its stability, prestige, and long-term capital preservation. However, rental yields are relatively modest, particularly when compared with northern cities. Investors are increasingly focussing on short-term rental opportunities in high-demand districts and properties that cater to tenants seeking flexibility and proximity to employment hubs.

Despite modest yields, London’s market remains resilient, benefiting from global investment flows and structural scarcity in key boroughs. We recommend that investors considering London approach with a long-term capital growth strategy, supplementing yield with selective location-based investment to achieve optimal returns.

2.3 Emerging Regional Hotspots

Beyond the established northern hubs, cities such as Sheffield, Newcastle, and Birmingham are experiencing rising institutional interest.

These locations are increasingly recognised for their blend of affordability, growth potential, and strong local economies, making them attractive alternatives to more mature markets. Growth is particularly notable in student accommodation and mixed-use developments, where regeneration projects, transport upgrades, and economic diversification are driving both rental demand and capital appreciation.

Sheffield, for example, has seen renewed momentum through large-scale regeneration programmes, including city-centre redevelopment and expansion of its advanced manufacturing district. Its two major universities underpin consistent demand for student housing, while the presence of global firms in engineering and healthcare reinforces demand for high-quality rental stock.

Newcastle, meanwhile, is consolidating its position as a digital and technology hub for the North East. With strong government and private-sector support for innovation clusters, the city has attracted a growing base of start-ups and established firms in the digital and life sciences sectors. This, coupled with rising student and young professional inflows, creates a dynamic rental market that offers yields competing favourably with traditional northern cities such as Manchester and Leeds.

Birmingham continues to benefit from its role as the UK’s “second city,” with HS2 and significant transport upgrades improving connectivity to London and the wider Midlands. Major mixed-use developments are reshaping the city centre, while a young and expanding population ensures ongoing demand across both residential and commercial segments.

Investors should pay close attention to areas benefiting from infrastructure investment, university expansions, and sectoral diversification, as these factors tend to underpin long-term resilience. By targeting these emerging hotspots early, investors can capture above-average yields while positioning themselves for sustained capital growth as these cities continue to evolve into established investment destinations.

3. Sector Analysis

3.1 Residential Sector

Residential investment in 2026 is characterised by three dominant sub-sectors.

City-Centre Apartments

These properties remain highly attractive to young professionals seeking proximity to employment hubs, transport links and lifestyle amenities.

Regeneration-led urban renewal is further boosting appeal, with new cultural, retail, and leisure facilities increasing the desirability of central locations. Investors are also seeing resilience in this segment despite economic uncertainty, as rental demand continues to outpace supply in most city centres.

Build-to-Rent Schemes

Increasingly popular in urban centres, build-to-rent (BTR) schemes are reshaping the rental market by offering tenants flexible lease structures, modern facilities, and professionally managed living environments.

For investors, BTR provides predictable rental streams, lower vacancy risk, and scalability across multiple cities. Demand is reinforced by structural shifts in housing affordability, with many renters opting for long-term tenancies over ownership. In key regional cities, the expansion of BTR is helping to meet chronic housing shortages while appealing to institutional investors seeking stable, long-term returns.

Student Housing

This sector continues to outperform others, particularly in cities with expanding university populations and limited supply of purpose-built accommodation.

Yields are high, vacancies remain consistently low, and long-term demand is underpinned by both domestic and international student inflows. Markets such as Birmingham, Sheffield, and Newcastle are emerging as hotspots for student housing investment, benefiting from university growth strategies and ongoing regeneration around campus areas.

As competition intensifies, investors are focusing on high-quality developments with strong amenities and proximity to universities, recognising that well-positioned student schemes can deliver both income stability and capital growth.

3.2 Commercial Sector

Grade A Office Space

Strong demand persists in northern hubs, particularly in Manchester and Leeds where many once-London based offices are relocating due to cheaper rents. Companies are seeking modern, energy-efficient and well-located facilities with robust transport links.

Occupiers are prioritising ESG-compliant buildings, flexible layouts, and proximity to talent pools, making Grade A developments the most resilient office sub-sector. While hybrid working has softened demand for secondary stock, high-quality office space in strategic locations continues to command premium rents and attract long-term corporate tenants.

Retail

Investment in the retail sector is increasingly selective, concentrated in prime city centre locations where tenant mix is diversified and footfall remains resilient.

Flagship shopping districts and well-curated retail destinations are seeing continued activity, often supported by mixed-use redevelopment that blends retail with residential and leisure. By contrast, secondary high streets continue to face structural pressures, with persistent vacancy rates and ongoing competition from e-commerce. Local authority-led regeneration and repurposing initiatives, such as converting excess retail space into residential or flexible commercial use, are expected to play a pivotal role in stabilising these areas.

In both office and retail segments, a focus on sustainability credentials, technological integration, and mixed-use potential is proving key to maintaining relevance. Data-driven analysis of occupancy trends, footfall, and regional economic activity is essential to mitigate risk, allowing investors to distinguish between resilient, income-generating assets and those exposed to structural decline.

4. Strategic Insights

Based on current trends, investors should consider the following approaches:

Diversify Regionally

Putting too much weight on London can limit yield potential and increase exposure to market swings. Northern cities such as Manchester, Leeds and Liverpool, along with rising hubs like Sheffield, Newcastle and Birmingham, are offering attractive returns supported by regeneration projects, new transport links and strong local economies. Spreading investments across regions helps balance risk while capturing growth in areas that are still on an upward trajectory.

Focus on Quality

Homes and offices that are newly built, recently refurbished or rich in modern amenities are consistently drawing premium rents and dependable tenants. Energy efficiency, sustainability and flexible layouts are becoming must-haves for occupiers. By focusing on high quality stock, investors are more likely to enjoy steady rental income, longer tenancy agreements and protection against future obsolescence.

Follow Tenant Trends

Shifts in lifestyle and work patterns continue to shape demand. Flexible working, a growing appetite for short-term rentals and the resilience of student housing are key drivers in 2026. Portfolios that adapt to these trends, whether through build-to-rent schemes with strong amenities or well-located student accommodation, are more likely to outperform and remain resilient in the long run.

Monitor Macro Factors

Changes in interest rates can quickly affect borrowing costs and net yields. Inflation, rising energy bills and new regulations also play a central role in shaping investment outcomes. Staying informed and building in flexibility allows you to respond to shifts in the wider economy and protect long-term portfolio performance.

Infographic suggestion: Checklist summarising the four strategic points.

5. Market Outlook for 2026 and Beyond

Looking ahead, northern cities are set to remain the primary growth engine for UK property investment. Their blend of strong rental demand, competitive yields, and long-term regeneration initiatives makes them highly attractive compared to more mature and expensive markets in the South.

Cities such as Manchester, Leeds, and Liverpool will continue to anchor investor activity, supported by infrastructure upgrades, university growth, and expanding employment bases in technology, healthcare, and finance. Alongside these established hubs, emerging regional centres including Sheffield, Newcastle, and Birmingham are gaining momentum, offering opportunities across both residential and commercial segments as they benefit from rising inward investment and public sector support.

For investors, the key considerations in 2026 can again be grouped into three broad themes.

Yield versus Growth

Investors face a balance between immediate income and long-term appreciation. Northern cities are particularly well placed to deliver both, offering yields above the UK average while also benefitting from regeneration-driven capital growth. By diversifying across established and emerging markets, investors can capture short-term rental performance while building exposure to areas with strong appreciation potential over the next decade.

Sector Selection

Performance will remain uneven across sectors. Residential apartments in central locations are set to remain resilient, particularly where demand is outpacing supply. Student housing continues to be one of the most consistent performers, underpinned by growing domestic and international university populations.

Grade A office space is expected to maintain momentum in northern hubs, with tenants prioritising modern, sustainable, and well-connected buildings. Retail, however, will remain highly polarised, with prime city-centre destinations attracting strong occupier interest while secondary high streets struggle to adapt to changing consumer behaviours. Investors who concentrate on sectors aligned with demographic trends and lifestyle shifts will be better placed to secure reliable, long-term returns.

Data-Led Decisions

In an increasingly competitive environment, data-driven strategies will be central to successful investment. City-level analysis, supported by comparative yield charts and mapping of regeneration corridors will help identify the most resilient sub-markets.

Understanding tenant demographics, infrastructure pipelines, and employment trends will allow investors to move beyond headline figures and pinpoint opportunities that offer both resilience and growth. Incorporating visual tools such as maps, comparative charts, and dashboards will also make it easier to track performance and adjust strategies as conditions evolve.

Taken together, these themes suggest that 2026 and beyond will be defined by regional strength and evidence-based decision-making. Investors who are prepared to look beyond London and embrace the opportunities in the North and other rising regional centres will be well positioned to achieve both stable income and long-term appreciation.

Conclusion

The UK property market in 2026 offers a blend of opportunity and risk.

Those who take a data-informed approach and focus on high quality developments while spreading their portfolios across regions are well placed to achieve strong yields and sustainable growth.

When wider economic trends are considered alongside local market knowledge and sector insight, it becomes easier to move with confidence and balance opportunity with risk. Northern cities stand out as compelling alternatives to London as they bring together higher yields, reliable tenant demand and clear potential for long-term appreciation.